Why DDR Corp is a Top Dividend Stock: A Juicy Yield of 9%

Today’s chart highlights one of the most common traits of a top dividend stock: a slumping stock price.

See, many analysts would have you believe that a stock is worth buying only if it has positive momentum working in its favor. In other words, they recommend that you buy “high” and sell “higher.”

Now, that kind of strategy might make sense if you’re a short-term trader looking to make a quick profit. However, if you approach stocks as a businessperson with long-term wealth-building in mind, there’s really only one time to buy: when they are cheap.

As regular readers know, I’m always on the prowl for a solid dividend stock that has been beaten down in price (for whatever reason). Why? Well, because if the company can somehow maintain or even grow its dividend payment amid the trouble, there’s a very good chance that the stock will rebound nicely over time. Before you know it, 10 years have passed and that very same stock has created huge wealth for you by providing steady income and huge price appreciation. It’s the stuff that stock market dreams are made of.

Well today, I’m highlighting real estate investment trust (REIT) DDR Corp (NYSE:DDR) as a top dividend stock with that kind of potential.

The Lowdown on DDR

For readers who haven’t heard about DDR before, it’s an owner and manager of “value-oriented” shopping centers. The company’s portfolio consists of 309 shopping centers, representing about 100-million square feet across 35 states and Puerto Rico.

Thus, DDR essentially acts a landlord to some of the biggest and most-well-known retail companies. It collects rent from these retail tenants and distributes it to shareholders in the form of juicy dividend payments.

Easy enough, right? Well, not exactly.

As you know, massive online competition–mainly from the behemoth known as Amazon.com, Inc. (NASDAQ:AMZN)–has put serious pressure on brick-and-mortar retailers. And many of DDR’s tenants are certainly no exception.

In fact, many of DDR’s tenants have already gone bankrupt recently, including the likes of sporting goods stores Sports Authority Inc and Golfsmith International Holdings Inc, as well as electronics retailer hhgregg, Inc. Naturally, these kinds of bankruptcies translate directly into vacancies and, in turn, lower income for DDR.

Unfortunately, the outlook isn’t significantly brighter for the rest of DDR’s portfolio. Take a look at this table of DDR’s top 10 tenants (by the % of its rental revenue):

| Tenant | % of Annualized Base Rental Revenues |

| TJX Companies Inc (NYSE:TJX) | 3.8% |

| Bed Bath & Beyond Inc. (NASDAQ:BBBY) | 3.4% |

| PetSmart, Inc. (NASDAQ:PETM) | 2.9% |

| Wal-Mart Stores Inc (NYSE:WMT) | 2.7% |

| Kohl’s Corporation (NYSE:KSS) | 2.4% |

| AMC Entertainment Holdings Inc (NYSE:AMC) | 2.3% |

| Best Buy Co Inc (NYSE:BBY) | 2.3% |

| Dicks Sporting Goods Inc (NYSE:DKS) | 2.2% |

| Ross Stores, Inc. (NASDAQ:ROST) | 2.0% |

| Michaels Companies Inc (NASDAQ:MIK) | 1.9% |

Source: “2016 Form 10-K,” DDR Corp, April 4, 2017.

Aside from Wal-Mart and maybe TJX, it’s tough to have much confidence about the long-term future of any DDR’s most important tenants. And it’s exactly that uncertainty that has Wall Street so bearish on the stock.

Not So Pretty On Paper

You can see the impact of the poor retail environment clearly in DDR’s recent operating results. In Q1, the company posted a loss of $59.8 million, or $0.16 per share. Furthermore, DDR’s same-store net operating income slipped 0.1%.

So given the company’s shaky tenant outlook and rough bottom line, why in the world do I believe it is a top dividend stock? There are a few reasons.

The first is that management is making solid progress on the things under its control. For example, the company’s annualized base rent actually increased 5.5% in Q1. Additionally, DDR sold 10 assets and two land parcels for a hefty $123.7 million during the quarter. So even though DDR’s accounting profits aren’t so great at the moment, its pricing power and financial position are holding very steady (if not improving).

“We are pleased to report ongoing progress lowering leverage, as well as organizational streamlining to fit the Company’s current operating scale and to partially mitigate an expected modest decline in property profitability this year,” said David Lukes, president and chief executive officer of DDR Corp. (Source: “DDR Reports First Quarter 2017 Operating Results,” DDR Corp, April 25, 2017.)

Cash Flow Still Fab

But of course, the biggest reason why I still believe in DDR is its strong cash flow generation.

After all, it is from a company’s free cash flow–not its accounting profits–in which dividends are paid to us shareholders. And when it comes to DDR’s dividend, it remains one of the safest in the retail REIT space.

In Q1, for instance, DDR still managed to produce operating funds from operations (FFO) (the most useful cash flow metric with REITs) of $108.5 million, or $0.30 per share. That’s only down slightly from $114.2 million in the year-ago period.

Meanwhile, the company distributed a dividend of $0.19 per share during the quarter, representing an FFO payout ratio of just 63%. That provides a firm cushion for management to maintain or raise the dividend even if the retail environment doesn’t improve much.

“I am confident DDR will emerge from a challenging 2017 well positioned to take advantage of an environment rich with opportunities arising from the current dynamic retail real estate markets,” Lukes said. (Source: Ibid.)

Top Dividend Stock at a Good Price

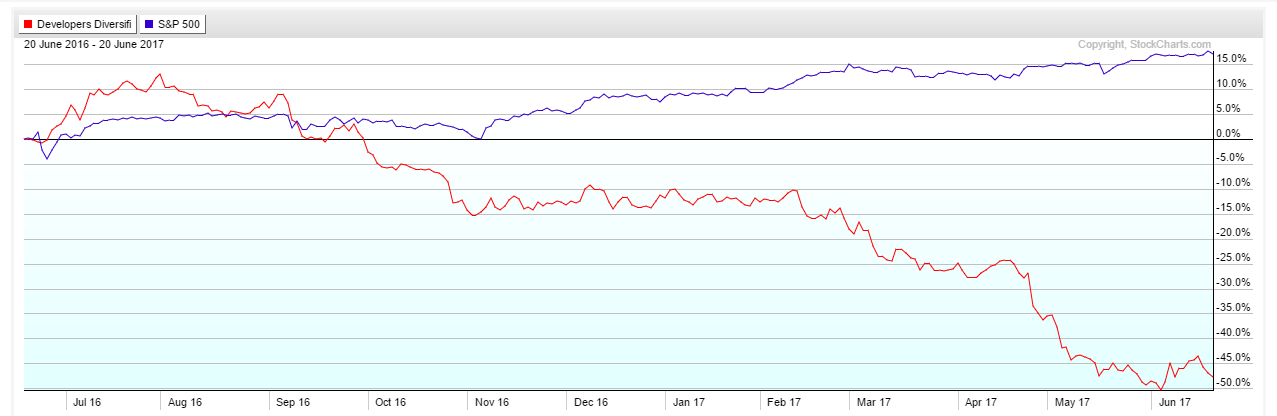

That brings us back to DDR’s stock price, which has been battered over the past year:

It’s tough to blame investors for giving up on DDR amid all of the retail wreckage. However, the company’s solid management team and well-covered dividend give me peace of mind.

In fact, DDR now boasts a rather scrumptious dividend yield of 9%. That is basically double the average yield of the retail REIT space (4.4%), and well above the S&P 500 (2.1%).

The Bottom Line on DDR Corp.

And there you have it: several reasons why I think DDR is a top dividend stock.

As is always the case, don’t view this article as a formal “buy” recommendation. Instead, see it as good starting point for more in-depth research. DDR stock is far from a stress-free stock and you need to be comfortable with the risks. That said, I believe the upside is definitely worth looking into.