Consider Wells Fargo Stock for Its Dividends

If you asked me to draw a sketch of the perfect dividend stock, it would probably look something like Wells Fargo & Co (NYSE:WFC) stock.

Wells Fargo is a bank, and a very old one at that. The company’s history can be traced back to the 1850s, when financiers and entrepreneurs flocked to California during the California Gold Rush. Today, Wells Fargo is the third-largest bank in the U.S., with $2.0 trillion in assets.

Now, I know what you’re thinking: with so many fast-growing companies trading in the stock market, why is a century-old bank the perfect dividend stock?

Well, the reason is simple. Well Fargo runs a timeless business. It has proven its value to investors over the past century. And going forward, I have every reason to believe that the company has no problem delivering strong returns for another 100 years.

Wells Fargo Stock: Running a Wonderful Business

Today’s banks come in all shapes and sizes. Despite being one of the biggest players in the industry, Wells Fargo’s business is incredibly simple. The bank makes most of its money from its lending business and service fees.

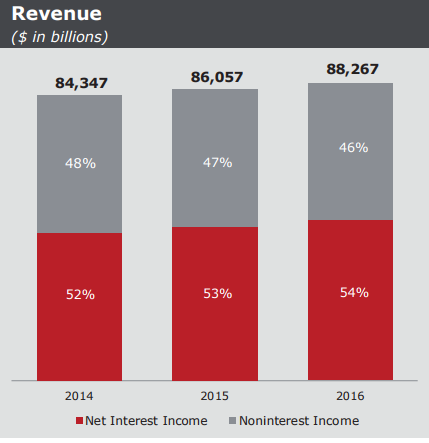

For centuries, banks have been lending money at higher interest rates than what they borrow at. It’s a wonderful business model that’s proven to work. What I like about Wells Fargo is that the company sticks to this business model. It doesn’t have a large investment banking segment or excessive trading operations. As the chart below shows, net interest income has consistently been the company’s number-one source of revenue.

In 2016, net interest income was responsible for generating 54% of Wells Fargo’s total revenue. In the first quarter of 2017, net interest income’s share of revenue has increased to 56%.

Source: “Financial Overview,” Wells Fargo & Co, last accessed July 7, 2017.

Earning interest income may look like a boring business compared to latest developments in “Fintech.” However, it is a business that has provided banks with recurring revenue through economic cycles, technology advancements, and even world wars.

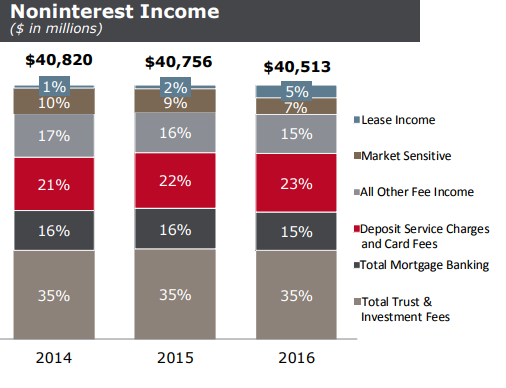

What about noninterest income?

Wells Fargo’s noninterest income includes deposit service charges, card fees, trust and investment fees, mortgage banking fees, market sensitive fees, and other fee income.

Source: “Financial Overview,” Wells Fargo & Co, last accessed July 7, 2017.

As you can see, the company has diversified sources of non-interest income, most of which is fee income. In particular, customer driven fees, such as deposit service charges and card fees, have increased due to the bank’s growing customer base.

Also Read:

WFC Stock: Warren Buffett Likes Wells Fargo & Co, Should You?

5 Dividend Bank Stocks that Will Keep Flying Under Trump

WFC Stock: Wide Economic Moats

Of course, since banking is such a wonderful business, others will want to enter the business too. Should Wells Fargo investors worry about competition?

Not really. Wells Fargo is deeply entrenched in the retail banking business. The company has more than 8,500 banking locations, 13,000 ATMs, and offices in 42 countries and territories. As a matter of fact, Wells Fargo is the number-one retail branch network in the U.S.

The established position of Wells Fargo provides it with a natural economic moat. In fact, the company is currently serving one-in-three households in America. If someone wants to compete with Wells Fargo, it would need to build an equally expansive branch network and convince millions of customers to switch. Ultimately, challenging Wells Fargo would be a very costly endeavor with no guarantee of success.

Thanks to its economic moat, Wells Fargo can keep making handsome profits. And since the company operates in a slow-changing industry, it doesn’t have to spend a whole lot on R&D. This means Wells Fargo stock can afford to return value to shareholders.

Mike Mozart/Flickr

The company currently pays $0.38 of dividends per share on a quarterly basis, giving Wells Fargo stock an annual dividend yield of 2.74%. Over the last five years, WFC stock’s quarterly dividend rate has increased 73.7%. (Source: “Stock Price and Dividends,” Wells Fargo & Co, last accessed July 7, 2017.)

The company is also buying back its shares. In the first quarter of 2017, Wells Fargo returned $3.1 billion to investors through dividends and share repurchases.

But the best could be yet to come. The company’s total loans and total deposits have been increasing, meaning its net interest income could see further growth down the road. And despite all the dividend hikes over the years, Wells Fargo’s payout ratio remains relatively low. Last year, the company’s dividend payout ratio was just 37.6%, leaving plenty of room for future dividend increases.

The Bottom Line on Wells Fargo Stock

In today’s market, there are plenty of companies with great growth prospects. Some say they are making the “next big thing,” and I have no doubt that some of these companies will turn out to be great investments. However, due to their risk, these companies are probably better suited for a speculative portfolio rather than an income one.

A stable and durable business is key to being a top dividend stock, and Wells Fargo has exactly that. With wide economic moats and the ability to return value to shareholders, Wells Fargo stock is a top pick for 2017 and beyond.