Western Midstream Partners LP: 12% Payout Keeps Growing

Is Western Midstream Partners LP’s 12% Yield Really Safe?

All high-yield stocks should come with a warning label: “Danger: These investments can be hazardous to your wealth.”

These stocks often represent troubled businesses with declining cash flows. It also means other investors looked over these businesses and took a pass. But once in a while, you find a rare company that offers both high quality and high yield.

Case in point: Western Midstream Partners LP (NYSE:WES). The pipeline sector has fallen out of favor on Wall Street, so even well-run companies now have big dividend yields. Western Midstream, which now sports a 12% yield, seems to fit into that category.

But can you really trust such an oversized payout? Savvy investors will want to dig into the financials before pulling the trigger on any high-yield stocks. Let’s dive into the numbers.

The first thing I check when evaluating a company’s dividend safety? Cash flow.

Generally, I like to see businesses pay out 90% or less of their profits as dividends. That leaves management with a little bit of wiggle room in the event of a downturn.

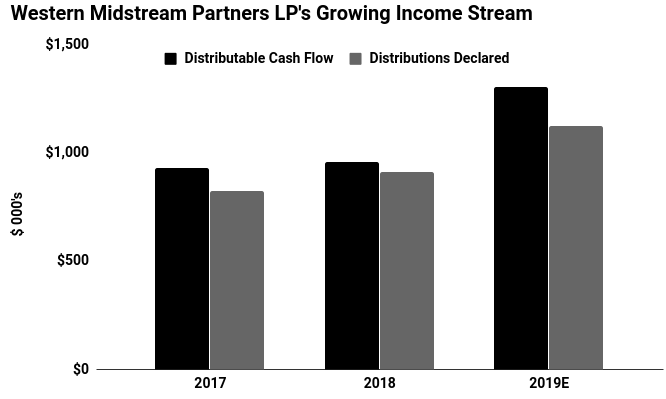

In the case of Western Midstream Partners LP, its executives have managed operations in a conservative manner. For 2019, the business is on track to pay out $0.86 in distributable cash flow for every dollar generated. That payout ratio sits well within my comfort zone.

The company’s cash flow seems to be growing, too.

New technologies have unlocked oceans of oil and natural gas from shale fields across the United States. But while oil and gas production booms nationwide, the industry doesn’t have enough infrastructure to physically ship, store, and process all of this energy.

Great news for Western Midstream. As a result of this energy boom, the partnership’s pipelines remain full. It also puts management in the position to jack up tolls on existing routes, padding the company’s bottom line further.

You can see this show up in the company’s financial results. Since 2017, Western Midstream Partners LP has seen its cash flow jump 41%. Moreover, analysts expect its income stream to continue growing at a low double-digit clip for the foreseeable future.

(Source: “Investors,” Western Midstream Partners LP, last accessed December 12, 2019.)

So, what could go wrong? The balance sheet.

To finance the partnership’s expansion, management has taken on a lot of debt. Today, Western Midstream has $4.50 in debt for every dollar generated in earnings before interest, taxes, depreciation, and amortization—on the high end for a pipeline business.

Such a leveraged balance sheet could force management to reduce the pace of dividend hikes. Executives might also look into selling some non-core assets to pare down the partnership’s debt load.

I don’t, however, expect this to jeopardize Western Midstream Partners LP’s distribution any time soon.