1 Large-Cap High Yielder to Consider

Large-cap stocks have been the bread and butter of many income investors’ portfolios. The reason is simple: for companies to command huge market capitalizations, they often need entrenched positions in their operating markets. And having an established market position allows companies to pay a steady dividend, which is exactly what income investors are looking for.

The thing is, though, many of these large-cap companies have also become household names. With huge followings in the stock market, their prices have already been bid up when markets rallied over the last several years. And because dividend yield moves inversely to share price, large-cap stocks are not known for offering the highest payouts. To give you some perspective, the average dividend yield of all S&P 500 companies stands at a measly 1.8% at the moment. (Source: “S&P 500 Dividend Yield,” Multpl.com, last accessed February 23, 2018.)

Today, however, I’m going to show you a large-cap stock that pays investors a much higher yield than its peers: Energy Transfer Partners LP (NYSE:ETP).

Also Read:

3 Mid-Cap Dividend Stocks Yielding Up to 10.45%

To the average consumer, Energy Transfer Partners may not sound like a familiar name. However, the partnership is deeply entrenched in its market. ETP owns and operates one of the largest and most diversified portfolios of energy assets in the U.S., which includes more than 71,000 miles of natural gas, natural gas liquids (NGLs), refined products, and crude oil pipelines, as well as over 210 billion cubic feet of working gas storage capacity.

The neat thing about the midstream energy business is that established players like ETP often have monopoly status in their operating regions. Energy pipelines are expensive to build, and once a set of pipelines is put in place and operating, it’s almost impossible to get the regulatory approval to build another one running side by side. In other words, it’s extremely difficult for a new company to enter the business and compete with ETP.

Furthermore, the business is largely fee-based. For instance, in Energy Transfer Partners’ Interstate Pipeline segment, approximately 95% of revenue is generated from fixed reservation fees, regardless of usage. In the partnership’s Midstream segment, approximately 80% of its fee-based margin comes from minimum volume commitment, acreage dedication, and throughput-based contracts. This helps limit the partnership’s exposure to commodity prices. (Source: “UBS Midstream & MLP Conference,” Energy Transfer Partners LP, last accessed February 23, 2018.)

With fee-based operations and a virtual monopoly status, Energy Transfer Partners is basically running a cash cow business. This allows the partnership to establish a quite generous distribution policy.

Right now, Energy Transfer Partners pays quarterly cash distributions of $0.565 per common unit, giving ETP stock an annual yield of 11.8%. In other words, investors purchasing ETP stock today can lock in a yield more than six times the benchmark S&P 500’s average.

Of course, one of the reasons behind the partnership’s ultra-high yield is the downturn in its unit price. Over the last 12 months, a period where all three major indices of the U.S. stock market surged past their all-time highs, ETP stock tumbled more than 20%. Ouch!

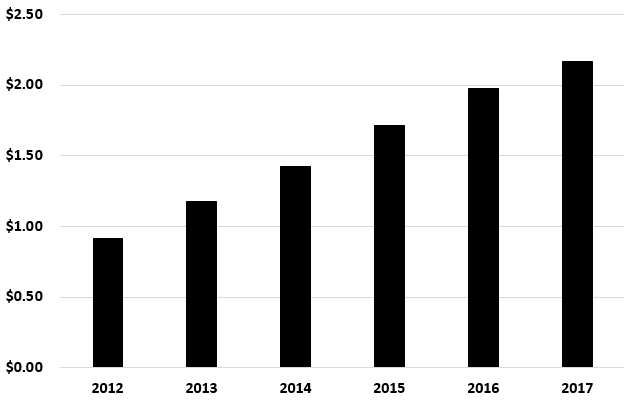

However, unlike the case with some beaten-down energy stocks, Energy Transfer Partners didn’t really cut back its dividend. The chart below shows the partnership’s distribution history for the past six years.

Energy Transfer Partners Distribution History

Source: “Distribution History,” Energy Transfer Partners LP, last accessed February 23, 2018.

As you can see from the chart, ETP’s distributions have been consistently increasing. Oil and gas prices plunged big time in the summer of 2014, leading to many dividend cuts in the energy sector. But ETP was still raising its payout. In fact, from its total cash distributions of $0.92 in 2012 to $2.17 paid in 2017, Energy Transfer Partners’ per share payout had grown by 135.9% over the six-year period.

Now, I know what you are thinking: with oil and gas prices yet to make a full recovery, isn’t this kind of dividend growth a bit too aggressive? Well, a look at the partnership’s financials should be reassuring.

Energy Transfer Partners reported earnings last week. In the fourth quarter of 2017, the partnership generated $1.20 billion in adjusted distributable cash flow, representing a 25% increase year-over-year. Since ETP declared and paid total cash distributions of $921.0 million for the quarter, it achieved a commendable distribution coverage ratio of 1.3 times. (Source: “Energy Transfer Partners Reports Fourth Quarter Results,” Energy Transfer Partners LP, February 21, 2018.)

In the full year 2017, ETP grew its adjusted distributable cash flow by 16% to $4.19 billion while declaring and paying total distributions of $3.49 billion. That translated to a distribution coverage ratio of 1.2 times, also leaving a sizable margin of safety.

Ultimately, it’s not every day that you find a large-cap stock with a double-digit payout. Due to ETP’s stable business model and solid financial profile, the recent pullback in unit price could represent an opportunity for yield-seeking investors.