Sabra Healthcare REIT Inc.: This 9.1% Yield Looks Compelling

Sabra Stock’s Yield Is 9.1% and Growing

To earn bigger yields, you have to get creative.

Blue-chip dividend stocks just don’t cut it anymore. To find income, dividend hunters need to scope out lesser-known niches—like business development corporations (BDCs) or master limited partnerships (MLPs).

Real estate investment trusts (REITs) are one of the last bastions of yield today. These firms buy properties and rent them out to tenants. And because they’re required by law to pay out most of their profits to investors, it’s not uncommon to find REITs paying yields as high as 12%, 15%, or even 17%.

One of my favorites: Sabra Health Care REIT Inc (NYSE:SBRA). The partnership doesn’t have the biggest following among income investors, but with a 9.1% yield and growing distribution, this could become one top dividend stock over the next decade.

Sabra owns a collection of specialty hospitals, transitional care facilities, and senior housing nationwide. Thanks to America’s aging population, these businesses enjoy high rents and low vacancy rates.

As a result, the partnership stands on a firm financial footing. Over the past 12 months, Sabra generated $2.31 per unit in adjusted funds from operations (AFFO) and paid out $1.73 per unit in distributions. This 75% payout ratio leaves management with plenty of wiggle room to keep making payments even in the event of a downturn.

That payout will likely continue to grow. Each year, 365,000 baby boomers turn 65; that’s larger than the population of Honolulu. With the demand for healthcare services exploding, rental prices for specialized medical facilities continue to grow.

Sabra has found itself right in the middle of this boom.

Over the past few years, management has plowed millions of dollars back into the business. This includes a number of growth initiatives, such as acquiring new buildings and renovating existing ones. Analysts project that these projects should allow the partnership to grow its cash flows at a high single-digit clip over the next five years.

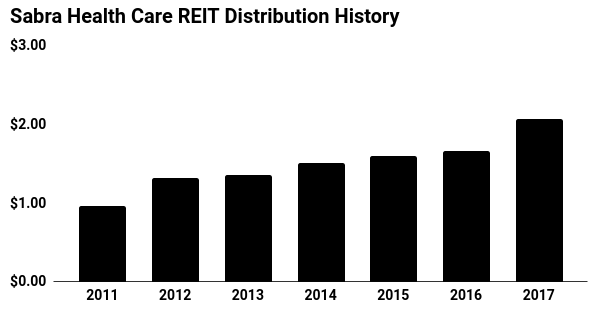

Most of these profits get passed onto unitholders. Since Sabra Healthcare began paying distributions in 2011, executives have boosted the payout on a regular schedule each year. As you can see in the chart below, those small, steady increases have created quite the stream of income.

(Source: Yahoo! Finance, last accessed August 10, 2018.)

The only thing that could upset this growth story would be higher interest rates.

That’s because REITs fund most of their business by borrowing copious amounts of cash. If interest rates rise, that would slow their pace of future acquisitions and, by extension, future distribution hikes.

That said, Sabra’s light debt load positions it well in a higher-interest-rate world. Soaring healthcare spending should also allow the partnership to grow earnings organically through rent hikes.

For those looking for a big upfront yield, Sabra Healthcare is one name to look into further.