Plains All American Pipeline Stock: High-Yielder Reported Earnings Growth of 44%

Why PAA Stock Is Worth Watching

Energy stocks were the biggest winners in 2021 and 2022.

Although 2023 started out slow for the oil and natural gas industry, crude oil prices have been climbing higher since June on the heels of record-high demand, production cuts by the Organization of the Petroleum Exporting Countries Plus (OPEC+), and—more recently—geopolitical tensions in the Middle East.

The U.S. Energy Information Administration (EIA) predicts that Brent crude oil, which is currently trading around $84.00 per barrel, will average $95.00 per barrel in 2024.

That bullish call is great news for Plains All American Pipeline (NYSE:PAA), which is one of the largest independent midstream energy companies in North America.

Plains All American provides logistics services to the crude oil, natural gas, and natural gas liquid (NGL) industry in the U.S. and Canada.

On average, the company handles about eight million barrels per day of crude oil and NGL through its extensive North American network, which is located in key producing basins, major market hubs, and transportation gateways. (Source: “Investor Presentation: Third-Quarter 2023,” Plains All American Pipeline, last accessed October 30, 2023.)

The company’s crude oil segment, which accounts for roughly 80% of its revenues, includes the following infrastructure:

- 18,300 miles of pipelines and gathering systems

- 74 million barrels of commercial storage

- Four marine facilities

- One condensate processing facility

- Seven rail terminals

- 2,100 railcars

- 640 trucks

- 1,275 trailers

(Source: “Crude Oil,” Plains All American Pipeline, last accessed October 30, 2023.)

Its NGL infrastructure includes:

- Four processing facilities

- Nine fractionation plants

- 28 million barrels of storage

- 1,620 miles of pipelines

- 16 rail terminals

- 3,900 railcars

- 220 trailers

(Source: “NGL,” Plains All American Pipeline, last accessed October 30, 2023.)

All that translates to:

- More than eight million barrels per day of total pipeline tariff volume

- More than six million barrels per day of Permian pipeline tariff volume

- About 135 million barrels per month of liquid (crude oil and NGL) storage capacity

- About 185,000 barrels per day of NGL fractionation capacity

(Source: “Investor Presentation: Third-Quarter 2023,” Plains All American Pipeline, op. cit.)

The company’s infrastructure is definitely not static. In February, it announced that it closed on the sale of its non-operated ownership interest in the Keyera Fort Saskatchewan facility to Keyera Corp (TSE:KEY, OTCMKTS:KEYUF) for about $271.0 million. (Source: “Plains All American Completes Divestiture of Interest in Keyera Fort Saskatchewan Facility,” Plains All American Pipeline, February 13, 2023.)

In July, a subsidiary of Plains Oryx Permian Basin LLC, which is a joint venture of Plains All American and Oryx Midstream Services Permian Basin LLC, closed a deal to acquire Diamondback Energy Inc’s (NASDAQ:FANG) 43% interest in OMOG JV LLC for about $225.0 million ($145.0 million net for Plains All American Pipeline’s interest). (Source: “Plains Adds Permian Basin Gathering Interests, Sanctions Canadian Expansion,” Oil & Gas Journal, August 4, 2023.)

Plains All American will hold a 65% interest in the joint venture and Oryx Midstream Services Permian Basin will hold a 35% interest.

The OMOG crude oil gathering and transportation system includes approximately 400 miles of crude oil gathering and regional transportation pipelines and 350,000 barrels of crude oil storage in Texas. The acquisition complements Plains All American Pipeline’s existing geographic footprint.

Moreover, the company said it was taking steps to improve the durability and quality of the cash flow in its NGL segment. This includes going ahead with improving the operational efficiency of its Fort Saskatchewan facility and extending the duration of its NGL contracts.

Q2 Net Income Up 44% Year-Over-Year

For the second quarter ended June 3, Plains All American announced that its net income advanced 44% year-over-year to $293.0 million. Its net cash provided by operating activities went up by 12% year-over-year to $888.0 million. (Source: “Plains All American Reports Second-Quarter 2023 Results and Provides Updated 2023 Guidance,” Plains All American Pipeline, August 4, 2023.)

The company generated second-quarter free cash flow (FCF) of $650.0 million, down slightly from $688.0 million in the second quarter of 2022.

For full-year 2023, Plains All American Pipeline expects that its adjusted earnings will be at the high end of its guidance range. Furthermore, the company is maintaining its 2023 investment and maintenance capital guidance of $325.0 million and $195.0 million, respectively.

Management expects to report $1.6 billion of FCF for full-year 2023. The company also expects to meaningfully increase its returns of capital to equityholders and further reduce its absolute debt.

Plains All American Pipeline Stock’s Q2 Distribution Increased 23%

Plains All American’s strong, reliable FCF generation allows it to implement its previously announced capital allocation framework, which is focused on increasing returns to unitholders and enhancing its financial flexibility.

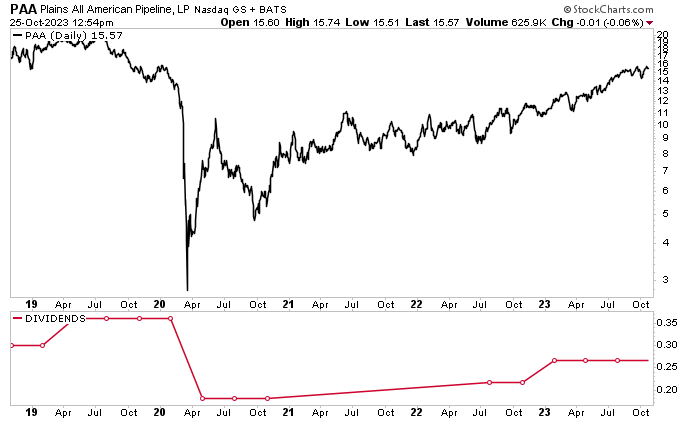

In October, the company declared a third-quarter distribution of $0.2675 per unit, for a yield of 6.87%. This payout represents a 23% increase over the $0.2175 that PAA stock paid out in the third quarter of 2022. (Source: “Plains All American Pipeline and Plains GP Holdings Announce Distributions,” Plains All American Pipeline, October 5, 2023.)

Plains All American Pipeline stock has one of the most reliable high-yield dividends in the energy sector. The company targets multiyear sustainable growth. And its dividend yield seriously outperforms every other sector in the S&P 500, which itself only has an average dividend yield of 1.6%.

That distribution growth is forecast to continue, with an expected three-year forward compound annual growth rate (CAGR) of 12.4%, compared to 3.6% for other master limited partnerships.

Moreover, PAA stock’s distribution is safe; the company’s payout ratio is just 59.88%.

PAA Units Thumping the S&P 500

Strong industry dynamics have helped Plains All American units trend steadily higher in price, easily outperforming the broader market. As of this writing, Plains All American Pipeline stock is up by:

- 23% over the last six months

- 40% year-to-date

- 42% year-over-year

Big gains, and more gains are expected. Wall Street analysts have provided a 12-month median share-price estimate for PAA stock of $17.00 and a high estimate of $20.00. This points to potential gains in the range of nine percent to 28%.

The high estimate would put Plains All American Pipeline stock at its highest level since July 2019.

Chart courtesy of StockCharts.com

The Lowdown on Plains All American Pipeline

Plains All American has been reporting terrific financial results, it has provided robust guidance, and—early this year—it raised its quarterly dividend by 23%. In terms of share price, PAA units have been crushing the broader market.

The company’s expansion in the Permian Basin, along with the high global demand for North American energy, bodes well for PAA stock’s price and reliable, high-yield dividends.