Northrop Grumman Corporation Investors Can Get Share of $738-Billion Windfall

Big, Safe Dividend Income From Northrop Grumman Corporation

Turkey invaded northern Syria. China threatened to attack Taiwan. Iran resumed the construction of nuclear weapons.

It’s a scary world out there (except to defense contractors).

America spends $738.0 billion a year on the military to keep our nation safe from threats—more money than the annual economic output of Switzerland. That straightforward figure represents a seriously big industry. (Source: “US budget boosts military spending,” Army Technology, July 23, 2019.)

But as the number of conflicts grows worldwide, that budget looks poised to balloon. Congress also needs to retire Cold War-era defense systems with the next generation of weapons like hypersonics, a technology where America has fallen behind rivals like China and Russia.

All of which means it’s a great time to be in the war business. Yes, some of the cash goes to pay and feed our troops. The bulk, however, ends up in the hands of corporations. Since 2014, the S&P Aerospace & Defense Select Industry Index has posted a gain of 130%. That beat the pants off the 89% bump in the S&P 500 over the same period. Record profits have also allowed the industry to pay out billions of dollars in dividends and buybacks.

One of the big winners from this boom is Northrop Grumman Corporation (NYSE:NOC). As one of the nation’s premier weapons makers, this company stands first in line to snag government contracts. Northrop Grumman secured $31.0 billion in sales in 2018 alone, and that number looks poised to grow in the years ahead. For investors, this has translated into a lucrative income stream. (Source: “2018 Annual Report,” Northrop Grumman Corporation, last accessed December 12, 2019.)

Let me explain.

Northrop Grumman Corporation was created in 1994 following a merger between two icons of the aerospace business, Northrup and Grumman.

Northrup can trace its roots back to World War II, when the company designed the U.S. Army Air Force’s “P-61 Black Widow” night fighter. In the Pacific theater, Grumman assembled the Navy’s “Cat” fighter planes.”

During the Cold War, both Northrup and Grumman worked on a variety of projects for the military, from fighter planes and stealth bombers to ballistic missiles and weather radars. Grumman even designed the “Apollo Lunar Module,” which landed on the moon.

Today, Northrop Grumman provides a wide range of services to the U.S. military.

Its “Missions Systems” division (33% of sales in 2019) provides the technology that commanders need in order to keep a bird’s eye view of the battlefield. Then there’s “Technology Services” (10%), which provides back-end logistical support, such as training, compliance, and data analysis. “Innovation Systems” (16%) manufactures satellites, ballistic missiles, and missile defense systems. This division also provides space-launch services, the equivalent to an interstellar taxi business, which analysts expect could bring in a large chunk of cash flows in the coming years. (Source: “Northrop Grumman Corporation October 2019,” Northrop Grumman Corporation, last accessed December 12, 2019.)

But Northrop Grumman’s core business remains aerospace. Altogether, the “Aerospace Systems” division accounts for 41% of the company’s sales.

These businesses gush profits for one simple reason: limited competition. Few companies have the know-how to design, develop, and manufacture military hardware. Fewer still have the insider knowledge to navigate Beltway politics and land government contracts. And almost nobody has the raw scale needed to actually build aircraft and weapons systems.

As a result, Northrop Grumman has only one or two competitors in most of the markets it competes in. In some cases, the business has a total monopoly. This allows the company to charge thick margins on new contracts, with little fear of being undercut by rivals.

But the best part? Government contracts often result in decades of recurring revenues. Once Northrop Grumman delivers a final product, the military still needs training, maintenance, and replacement parts. Once again, few companies have the know-how to build new flaps for a stealth bomber or infrared cameras for an attack drone. And when American lives are on the line, how many generals want to take a chance on an upstart company?

For this reason, Northrop Grumman can charge an arm and a leg to maintain weapon systems as long as they remain in service. It’s like owning an annuity of cash flow.

You can see the profitability of this business in the company’s financial statements. Last year, its margins topped 12%. Over the past decade, Northrop Grumman has averaged $0.13 in profit on every dollar that shareholders have invested in the business.

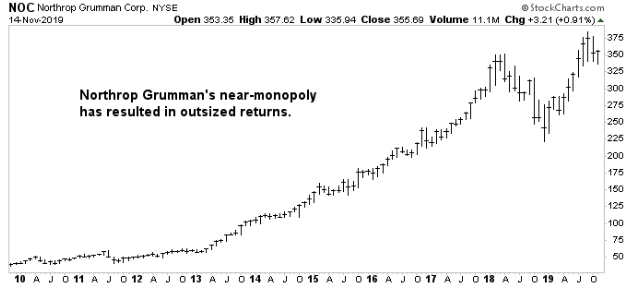

Chart courtesy of StockCharts.com

Some companies manage to earn returns like this once in a while. Over time, however, competition tends to take a bite out of those margins. By sustaining such high returns over a long period, Northrop entered the ranks of some of the most elite businesses in the world.

What does management do with all of this money? For the most part, they return it to shareholders.

Northrop Grumman has a ravenous appetite for its own stock. The company spent $3.2 billion on share buybacks in 2015, $1.6 billion in 2016, $393.0 million in 2017, and $1.3 billion in 2018. For 2019, management is on track to spend another $2.0 billion on this program.

This habit of repurchasing stock cuts the number of outstanding shares over time. Think of a business like a pizza. If you reduce the number of slices, each individual slice gets bigger. By buying back boatloads of stock, loyal investors can claim a bigger piece of future profits. And that, by extension, makes each share more valuable.

In the case of Northrop Grumman, steady, ongoing stock buybacks have cut the number of outstanding shares in half since 2003. (Source: (Source: “Northrop Grumman Corporation October 2019,” op. cit.)

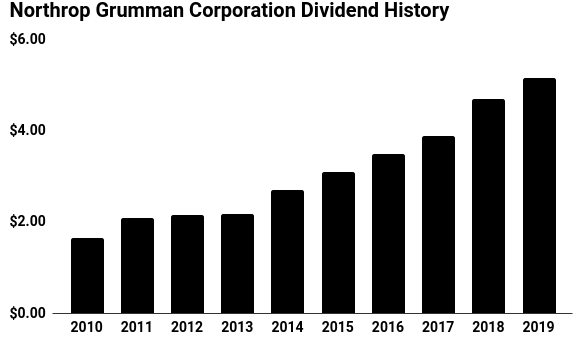

NOC stock pays cash dividends, too. The company has mailed a check to shareholders every year since its creation in 1994. And management has boosted this payout on an annual basis since 2002. Even through the last financial crisis, Northrop Grumman continued increasing its distribution to investors.

(Source: “Stock Information – Stock Split & Dividend Info,” Northrop Grumman Corporation, last accessed December 9, 2019.)

Now, at this point, you might be thinking, “So what could go wrong here?” With a near-perfect dividend track record, I see three big risks for the company: cost overruns, economic booms, and lower defense spending.

Beltway politics presents the biggest challenge. Northrop Grumman earns most of its revenues from the U.S. Department of Defense. So a leftward shift in D.C. or a change in Pentagon priorities could burn shareholders.

To be fair, a Democratic White House doesn’t necessarily spell disaster for defense contractors. The industry boomed under President Barack Obama. Northrop Grumman’s management has also addressed this problem by trying to sell its wares to new countries. Still, it’s a risk worth keeping an eye on.

The other issues look more mundane. Northrop Grumman controls costs by avoiding projects that have razor-thin margins, thereby leaving management with some wiggle room. We saw this recently when the company dropped out of the running to build the “T-X” jet trainer and the “MQ-25 Stingray” unmanned refueling drone.

A strong economy, as odd as it might sound, could also clip the NOC stock price. Because investors prize defense contractors for their recession-proof profits, they rotate into these names during economic downturns. This process, however, works in reverse during good times. But an economic boom wouldn’t have any impact on shareholder dividends, so any such sell-off could present an investment opportunity.

Bottom line: war is an ugly business. But as long as conflict exists, the U.S. government will continue to rely on defense contractors. And with our adversaries catching up to America’s military supremacy, cash outlays for research and development will probably grow. That likely means higher profits (and higher dividends) for Northrop Grumman Corporation shareholders.