Leggett & Platt Stock a Battered Dividend King for Contrarian Investors

7.1%-Yield LEG Stock Could Provide Big Returns

Dividend kings are companies that have raised their dividends for at least 50 consecutive years.

But not all dividend kings are created equal. While many of them are generally solid companies, some of them face difficulties. The question is how they respond to those difficulties.

Investors who seek contrarian opportunities and who are willing to be patient while collecting dividends should take a look at Leggett & Platt Inc (NYSE:LEG).

The diversified company manufactures engineered components and products for homes and automobiles. It has been around for 140 years and has an expansive global footprint comprising 35 manufacturing facilities in 18 countries. (Source: “Investor Relations,” Leggett & Platt Inc, last accessed January 11, 2024.)

Leggett & Platt’s products include:

- Adjustable beds

- Private-label finished mattresses

- Specialty bedding foams

- Bedding components

- Bedding industry machinery

- Home furniture and work furniture components

- Flooring underlayment

- Automotive seat support and lumbar systems

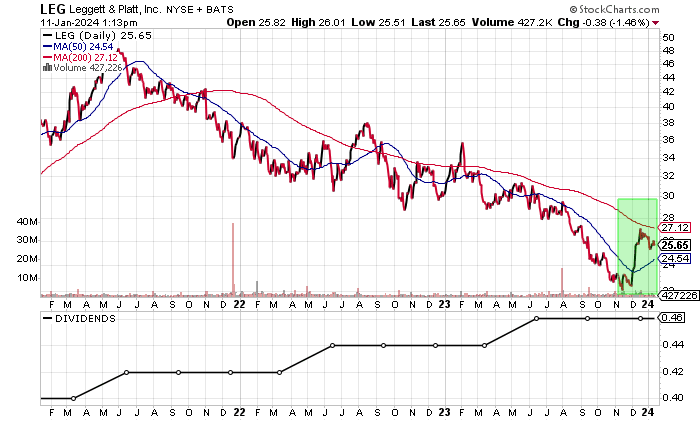

Leggett & Platt Inc has raised its dividends for 52 straight years, but its share price has been under pressure lately. As of this writing, it’s down by 28% over the past year and 57% from its record high of $59.16 in May 2021.

At the moment, Leggett & Platt stock is struggling for support. Its chart is flashing a death cross, which is a bearish technical crossover pattern that appears when the 50-day moving average (MA) breaks below the 200-day MA.

LEG stock recently overtook its 50-day MA of $24.75, which is encouraging. Reclaiming the 200-day MA of $28.01 would be a bullish sign.

Chart courtesy of StockCharts.com

Leggett & Platt Inc Is a Work in Progress

Leggett & Platt’s five-year revenue picture shows growth in four of its last five reported years, including a 10-year best of $5.15 billion in 2022.

The company has easily surpassed its pre-pandemic revenue level, but there are some headwinds coming. Analysts estimate that Leggett & Platt Inc will report lower revenues of $4.72 billion for 2023, followed by $4.72 billion again for 2024. (Source: “Leggett & Platt, Incorporated (LEG),” Yahoo! Finance, last accessed January 11, 2024.)

| Fiscal Year | Revenues (Billions) | Growth |

| 2018 | $4.27 | N/A |

| 2019 | $4.76 | 11.43% |

| 2020 | $4.28 | -9.97% |

| 2021 | $5.06 | 18.26% |

| 2022 | $5.15 | 1.66% |

(Source: “Leggett & Platt Inc.” MarketWatch, last accessed January 11, 2024.)

On the bottom line, Leggett & Platt has delivered generally accepted accounting principles (GAAP) profits, but the lack of consistent growth has hurt the company.

The outlook for the company’s GAAP-diluted earnings per share (EPS) is tepid. Analysts expect Leggett & Platt Inc to report a drop in its earnings to $1.39 per diluted share for 2023, prior to a slight rebound to $1.40 per diluted share for 2024. (Source: Yahoo! Finance, op. cit.)

The company has plenty of work ahead of it to rectify the situation. This is where patience will be required.

| Fiscal Year | GAAP-Diluted EPS | Growth |

| 2018 | $2.26 | N/A |

| 2019 | $2.47 | 9.3% |

| 2020 | $1.86 | -24.7% |

| 2021 | $2.94 | 58.1% |

| 2022 | $2.27 | -22.8% |

(Source: MarketWatch, op. cit.)

Leggett & Platt Inc’s funds statement shows consistent positive free cash flow (FCF) in all five of its last five reported years, including a strong FCF performance in 2022.

In 2022, the company bought back $60.3 million worth of its own common and preferred stock and paid $229.2 million to common shareholders.

| Fiscal Year | FCF (Millions) | Growth |

| 2018 | $280.7 | N/A |

| 2019 | $524.9 | 87.0% |

| 2020 | $536.4 | 2.19% |

| 2021 | $164.7 | -69.3% |

| 2022 | $341.1 | 107.1% |

(Source: MarketWatch, op. cit.)

A slight risk for Leggett & Platt Inc is its debt of $2.18 billion (as of the end of September 2023). The company does, however, hold $273.9 million in cash. (Source: Yahoo! Finance, op. cit.)

Leggett & Platt has easily covered its interest expense via higher earnings before interest and taxes (EBIT) from 2020 through 2022. The company’s interest coverage ratio in 2022 was a healthy 5.7x.

| Fiscal Year | EBIT (Millions) | Interest Expense (Millions) |

| 2020 | $410.6 | $82.7 |

| 2021 | $598.6 | $76.5 |

| 2022 | $489.1 | $85.5 |

(Source: Yahoo! Finance, op. cit.)

Leggett & Platt Inc’s Piotroski score—an indicator of a company’s balance sheet, profitability, and operational efficiency—is a fair reading of 4.0. That’s just below the midpoint of the Piotroski score’s range of 1.0 to 9.0.

Leggett & Platt Stock’s Dividend Should Be Safe

Leggett & Platt declared a quarterly dividend of $0.46 per share for the fourth quarter of 2023. (Source: “Dividends & Splits,” Leggett & Platt Inc, last accessed January 11, 2024.)

That represents a forward yield of 7.1% (as of this writing).

LEG stock’s higher dividend yield versus its five-year average yield of 4.46% is due to share-price deterioration. The company’s dividend coverage ratio of 2.5 times suggests that its dividend streak should stay intact.

| Metric | Value |

| Dividend Growth Streak | 52 Years |

| Dividend Streak | 53 Years |

| 7-Year Dividend Compound Annual Growth Rate | 4.7% |

| 10-Year Average Dividend Yield | 4.3% |

| Dividend Coverage Ratio | 2.5x |

The Lowdown on Leggett & Platt Inc

Make no mistake, Leggett & Platt has tons of work ahead of it to right its ship.

It’s not going to going to be easy, but Leggett & Platt stock’s share-price deterioration, along with its consistent dividends, will help compensate for some of the risk of holding LEG stock.