Inter Pipeline Ltd: This Energy Stock Gushes an 8.2% Yield

Can You Trust Inter Pipeline Ltd’s 8.2% Dividend Yield?

Are you looking for bigger dividend yields? Then you want to own the “toll bridge” of the energy industry.

If you own an oil company, then you often need to ship your production through pipelines from Point A to Point B. These routes serve as the “toll bridges” of the energy patch. And just like toll bridges, the businesses that own these pipelines collect their fee income again and again.

Case in point: Inter Pipeline Ltd (OTCMKTS:IPPLF, TSE:IPL). This Canadian company owns 4,800 miles of pipeline transporting over 1.4 million barrels of crude per day. Management has also acquired other assets over the years, including dozens of terminals, storage tanks, and processing plants.

Such profitable operations allow executives to fund an eight-percent dividend yield. But can such a high payout possibly be safe?

Is This Payout Safe?

Inter Pipeline Ltd manages its operations in a conservative fashion.

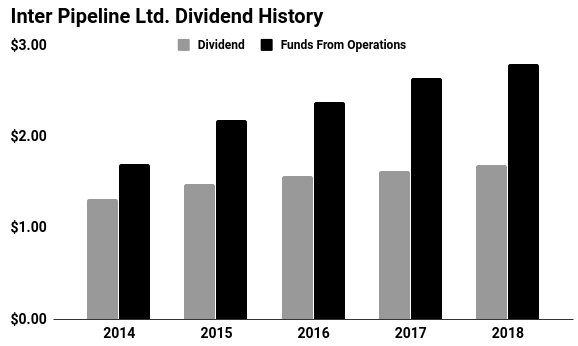

Last year, the business generated $2.80 per share in funds from operations. Over the same period, executives paid out $1.68 per share in distributions. (Source: “Inter Pipeline Announces Record 2018 Financial and Operating Results,” Inter Pipeline Ltd, February 14, 2019.)

Generally, I like to see companies pay out 90% or less of their profits. That leaves executives with a little bit of wiggle room to maneuver in a downturn. So Inter Pipeline Ltd’s 60% payout ratio sits well within my comfort zone.

That same conservatism applies to the balance sheet, too. The business has only $6.00 in debt for every dollar generated in earnings before interest, taxes, depreciation, and amortization (EBITDA). Management has also locked in most of those liabilities through fixed, long-term debt issues.

Those cash flows will likely continue to grow, too.

While Canada’s oil sands struggle with low energy prices, the industry continues to add incremental production. More barrels flowing through its network will translate into higher fee income for Inter Pipeline.

New investments should also boost cash flows. Last year, management started construction on the Heartland Petrochemical Complex. The $3.5-billion plant, located in the western province of Alberta, will convert approximately 22,000 barrels per day of low-cost, locally sourced propane into 525,000 tonnes of high-value polypropylene per year.

Wall Street seems optimistic. Over the next five years, analysts project Inter Pipeline will grow funds from operations at a high single-digit annual clip. Given the company’s low payout ratio, executives could boost the dividend at an even faster rate.

Source: “Annual Review 2018,” Inter Pipeline Ltd, last accessed May 9, 2019.

The Bottom Line on Inter Pipeline Ltd

So can you call Inter Pipeline a slam dunk? Not yet.

The Canadian oil sands, which the company serves, have fallen out of favor. Low energy prices have made new investment unprofitable, limiting growth in the region.

That said, Inter Pipeline makes money on the number of barrels flowing through its network, not necessarily on the price of those barrels. So while investors have fled the Canadian oil patch, pipelines continue to make money hand over fist. That has resulted in reliable dividends for shareholders.

That’s the benefit of owning a toll bridge.