Earn a Double-Digit Yield from This High Dividend Stock

When you see a high yield stock in today’s market, you might be wondering whether the company is going to cut its payout soon. And while double-digit yielders are not exactly known for their dividend safety, this high dividend stock’s payout is actually rock-solid.

In fact, investors who put their money in this company today may see even bigger dividend checks in the near future because of the growing amount of cash the business generates.

I’m looking at Energy Transfer Partners LP (NYSE:ETP), a master limited partnership headquartered in Dallas, Texas. Energy Transfer started in 1995 as a small intrastate natural gas pipeline operator. Today, it is one of the largest midstream MLPs in the U.S. with more than 71,000 miles of natural gas, natural gas liquids (NGLs), crude oil, and refined products pipelines.

Now, I know what you are thinking. In recent years, the energy sector wasn’t really known for its dividend safety. As a matter of fact, since the downturn in oil and gas prices started in the summer of 2014, quite a few energy firms have cut back their dividends.

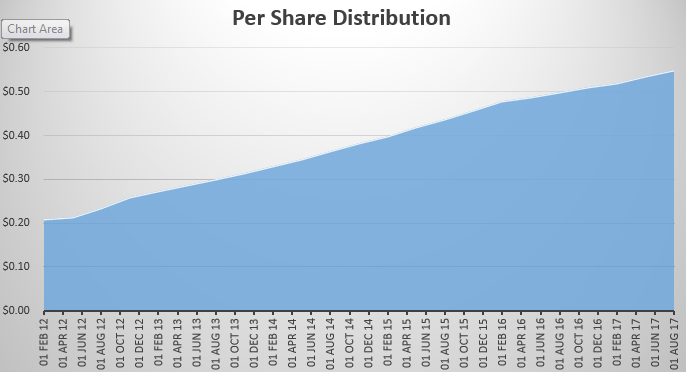

But that’s exactly why this high dividend stock is special. Not only did Energy Transfer Partners not cut its payouts, but it was actually raising them. The chart below shows the partnership’s per share distribution history for the past five years.

ETP Stock Dividend History

(Source: “Distribution History,” Energy Transfer Partners LP, last accessed August 11, 2017.)

In the beginning of 2012, Energy Transfer’s per unit distribution rate was $0.21. Today, the amount has risen to $0.55. That’s an increase of 162%!

In fact, Energy Transfer has raised its per unit payout at least once a year for the past 15 years.

How is it possible that a large energy partnership can keep raising its dividends even though everything else in the sector was deep in the doldrums?

The answer lies in the nature of ETP’s business. You see, the partnership is not in the exploration or production side of the energy business. Instead, it earns a fee to move and store energy products for other companies.

In other words, Energy Transfer Partners operates what are essentially toll roads and storage depots for energy products. And because it is not drilling new wells, the partnership doesn’t have to worry too much about the price of oil.

Furthermore, most of ETP’s midstream services are done through long-term, fee-based contracts. This adds stability to its cash flow, which is another reason why the partnership can afford to pay generous distributions.

Also Read:

7 Energy Stocks That Pay Healthy Dividends

MLP Stock List: Earn Reliable Income from These Energy Partnerships

And if you are wondering whether those oversized dividend checks are sustainable, a look at the partnership’s financials should be reassuring. ETP reported earnings earlier this month. In the second quarter of 2017, the partnership’s distributable cash flow grew 21% year-over-year to $990.0 million, providing 1.18 times coverage of its distributions. For the first half of 2017, ETP’s distribution coverage ratio was 1.15 times. This means the partnership is not paying out all the cash it generates, leaving a margin of safety. (Source: “Energy Transfer Partners Reports Second Quarter Results,” Energy Transfer Partners LP, August 8, 2017.)

At the current price, ETP’s dividend yield is 11.2%. In the most recent investor presentation, the partnership said that it is targeting a distribution growth rate in the low double digits. So for investors of this high dividend stock, the best could be yet to come.