Should Income Investors Consider This High-Yield Stock?

Risk-averse income investors tend to like large-cap stocks. Because large-cap companies usually have established operations and entrenched market positions, they can provide shareholders with a steady stream of dividend income.

However, because of their elite status in the investment world, large-cap stocks have always been highly sought after. As a result, investors have already bid up their prices, causing their yields to drop. In this day and age, a company with a four percent payout would proudly brand itself as a high-yield stock.

And that’s why Energy Transfer Partners LP (NYSE:ETP) deserves your attention. Commanding a market capitalization of over $22.0 billion, ETP is no doubt a large-cap stock. And yet it manages to offer investors a jaw-dropping yield of 11.7%.

Of course, at a given quarterly payout, a company’s dividend yield moves inversely to its share price. Therefore, beaten-down stocks can offer some of the highest yields.

Indeed, ETP stock hasn’t really been a hot commodity, due to its involvement in the energy sector. Since oil and gas prices crashed in the summer of 2014, the partnership has lost quite a bit of its market value.

The thing is, though, while ETP is an energy stock, it still runs a rock-solid business. And because the market hasn’t warmed up to the partnership, its high dividend yield could represent an opportunity for income investors. Let me explain.

ETP Stock: A Rock-Solid Business

Headquartered in Dallas, Texas, ETP is a master limited partnership (MLP) with a diversified portfolio of energy assets in the United States. The partnership owns and operates approximately 61,000 miles of natural gas pipelines, 146 billion cubic feet of working storage capacity, and over 60 natural gas facilities. (Source: “2018 MLP & Energy Infrastructure Conference,” Energy Transfer Partners LP, last accessed June 13, 2018.)

Through these assets, ETP provides natural gas processing, compression, treating, and transportation services.

At the same time, due to its 100% interest in Lone Star, Energy Transfer Partners has 2,000 miles of natural gas liquid (NGL) transportation pipelines and four NGL facilities.

Last year, Energy Transfer Partners merged with Sunoco Logistics Partners. The deal allowed ETP to add approximately 8,600 miles of crude oil, NGL, and refined product pipelines and associated storage to its portfolio. Through Sunoco Logistics, the partnership provides crude oil, NGL, and refined product transportation, terminaling, and marketing.

The key to note here is that ETP has an entrenched position in a market with high barriers to entry. Pipeline construction not only is extremely expensive, but also needs regulatory approval. After one pipeline system is put in place and operating, regulators usually won’t approve a proposal to build another pipeline running side by side.

With tens of thousands of miles of pipelines, Energy Transfer Partners has monopoly status in many of its operating regions.

Moreover, once up and running, pipelines don’t require a lot of maintenance capital. Operators like ETP can just sit back and enjoy the cash flow rolling in.

The energy “toll road” business has allowed the partnership to generate a fee-based operation. Because Energy Transfer Partners does not drill new wells, it doesn’t have to worry too much about commodity prices.

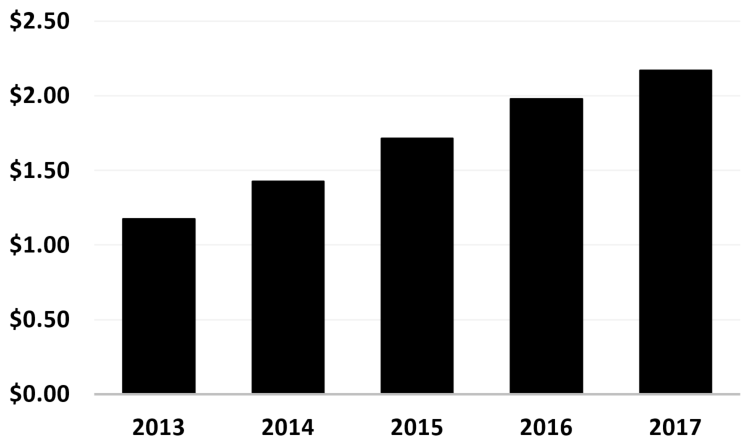

Energy Transfer Partners Distribution History

For investors, Energy Transfer Partners’ fee-based business mix has translated to an increasing income stream.

(Source: “Distribution History,” Energy Transfer Partners, last accessed June 13, 2018.)

In 2013, the partnership declared and paid total dividends of $1.17 per unit. In 2017, the amount stood at $2.17 per unit. That represented an increase of over 85%, which is quite impressive, given the downturn in oil and gas prices during this period.

And if you are concerned about this double-digit yielder’s dividend safety, don’t worry. Despite consistently raising its distributions in a volatile commodity price environment, Energy Transfer Partners still makes more than enough money to cover its payout.

In the first quarter of 2018, ETP generated adjusted earnings before interest, tax, depreciation, and amortization (EBITDA) of almost $1.9 billion, representing a 30% increase year-over-year. (Source: “Energy Transfer Partners Reports First Quarter Results,” Energy Transfer Partners LP, May 9, 2018.)

Distributable cash flow, a critical measure of an MLP’s performance, came in at $1.2 billion for the quarter, also up nearly 30% from the year-ago period. And since Energy Transfer Partners paid total distributions of less than $1.1 billion during the quarter, it achieved a distribution coverage ratio of 1.15 times, leaving a sizable margin of safety.

The Bottom Line on Energy Transfer Partners LP

To sum up, Energy Transfer Partners LP is a rare find in the energy sector. The partnership has provided increasing distributions in an era when dividend cuts were common among energy stocks. ETP stock also offers a yield that is substantially higher than the vast majority of its large-cap peers. And since the payout remains safe, the stock’s 11.7% yield looks like an opportunity for income investors.