Earn a Double-Digit Yield from This Top Dividend Stock

For dividend investors who want to boost the yield of their portfolios, this company deserves special attention.

It offers a double-digit dividend yield and has raised its payout in each of the last 15 years.

I’m talking about Energy Transfer Partners LP (NYSE:ETP), a master limited partnership (MLP) headquartered in Dallas, Texas.

For those not in the know, MLPs are publicly traded partnerships usually come from the energy sector. They are required by law to distribute almost all their available cash to investors in the form of dividends. In return, MLPs are exempt from corporate income tax.

Due to the mandatory distribution requirement and the tax-pass-through structure, MLPs have become the higher-yielding stocks in today’s market.

With a market cap of nearly $24.0 billion, Energy Transfer Partners is one of the largest MLPs in the country.

Of course, the reason why most investors haven’t really considered MLPs is their involvement in the oil and gas business. Since the downturn in commodity prices started in the summer of 2014, many energy companies—including some of the largest ones—have seen their financials deteriorate. Massive layoffs and dividend cuts were not uncommon.

For dividend investors, and particularly retirement investors who want to use their portfolio income to cover day-to-day expenses, few things are worse than a dividend cut.

However, Energy Transfer Partners has been an exception. To see why ETP stock is special, all you need to do is to take a look at its distribution history.

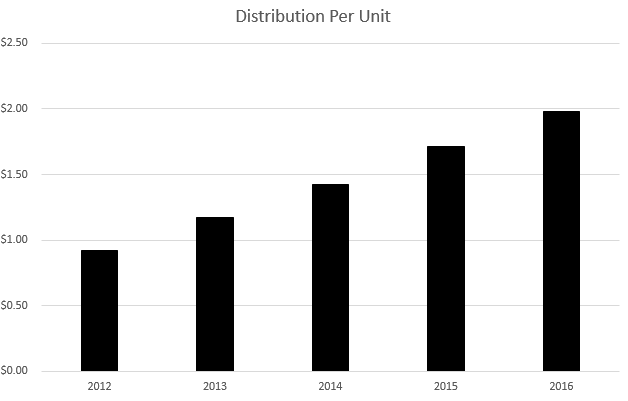

Energy Transfer Partners Distribution History

Source: “Distribution History,” Energy Transfer Partners LP, last accessed September 15, 2017.

In 2012, the partnership paid $0.92 of total cash distributions per unit. In 2016, the amount was $1.98 per unit; that’s an increase of 115%. So Energy Transfer Partners not only survived the downturn in oil and gas prices, but was actually raising its payout to investors when everything else was deep in the doldrums. As a matter of fact, the partnership has increased its dividend every year for 15 consecutive years.

Energy Transfer Partners is continuing its track record. In July, the partnership announced a $0.015 increase to its quarterly cash distribution rate to $0.55 per common unit. That’s an annualized payout of $2.20 per unit. At the current price, the partnership has an annual dividend yield of 11.6%. (Source: “Energy Transfer Partners Announces Quarterly Cash Distribution,” Energy Transfer Partners LP, July 27, 2017.)

A Fee-Based Business

The reason why ETP can pay an increasing dividend through thick and thin lies in the nature of its business. While the partnership operates in the energy sector, it focuses on the transportation and storage of oil and gas, rather than the production.

In the natural gas segment, the partnership operates approximately 61,000 miles of natural gas pipelines, 146-billion cubic feet of working storage capacity, and another 2,000 miles of natural gas liquids (NGL) transportation pipelines and 51-million barrels of NGL storage capacity.

rickz/Flickr

Energy Transfer Partners also has a sizable crude oil operation due to its interest in Sunoco Logistics. The operation includes approximately 8,600 miles of crude oil, NGL, and refined products pipelines and associated storage terminals.

In other words, the partnership does not have any drilling operation. It generates most of its cash flows through fee-based operations. In the crude oil segment, ETP earns fee-based revenue from the transportation and storage of crude oil. In the interstate natural gas transportation and storage segment, the partnership generates around 95% of cash flows through firm reservation charges, meaning its customers pay a fee to reserve capacity, regardless of usage. In the NGL and refined products business, transportation revenue comes from dedicated capacity and take-or-pay contracts. So customers either use ETP’s pipelines to move NGLs and refined products or pay a penalty specified in the contract.

By running a business that’s largely fee-based, ETP can generate stable cash flows, despite the volatile commodity price environment.

Also Read:

The Best Pipeline Stocks for Retirement Income

Pipeline Stock List Giving Reliable Dividends

Solid Financials

Of course, as dividend investors are well aware, a high yield can sometimes be a sign of trouble. However, despite being one of the highest-yielding large-cap stocks in today’s market, ETP’s payouts are actually backed by solid financials.

For a master limited partnership, a key metric to look for is distributable cash flow, because that’s where dividends come from. In the second quarter of 2017, ETP generated $990.0 million in distributable cash flow, representing an increase of $175.0 million from the year-ago period. (Source: “Energy Transfer Partners Reports Second Quarter Results,” Energy Transfer Partners LP, August 8, 2017.)

In the second quarter, Energy Transfer Partners achieved a distribution coverage ratio of 1.18 times. This means it was not paying out all the cash it earned, leaving a margin of safety. In the first six months of 2017, ETP’s distribution coverage ratio was 1.15 times.

Final Thoughts on ETP Stock

At the end of the day, keep in mind that there is still a lot of uncertainty about the future of oil and gas prices. But with a stable fee-based business, Energy Transfer Partners is well positioned to keep delivering returns to dividend investors.