This Company is Set to Return More Cash to Investors

Today’s chart highlights one of my favorite types of businesses, “virtual monopolies.”

In Economics 101, we learned that under perfect competition, firms cannot earn oversized profits in the long term.

That’s why analysts are always trying to identify companies with competitive advantage. When a company has a competitive advantage, it can differentiate itself from the competitors.

For instance, if a company manages to make a superior product, it might be able to corner the market and earn bigger profits, even in the long run.

In fact, investing in companies with durable competitive advantages is one of the key reasons behind Warren Buffett’s astronomical returns over the decades.

And it gets even better.

There is a small group of companies with competitive advantages so strong and so durable that there is virtually no competition.

Moreover, they are completely legal. There’s no antitrust law to worry about.

As a matter of fact, in some cases, the government even encourages these companies to be the only operator in their respective markets.

The best part is, you don’t need to travel to the end of the world to find these businesses. Some of them are operating right before our eyes.

Think about the toll road you last traveled on. The company operating that toll road has virtually no competition to worry about. That’s because once a toll road is built, it’s extremely unlikely that the government would approve the plan to build another toll road running side by side.

And then look at your natural gas distributor. If you want to heat your homes, you have no choice but making payments to that company. This is because in any given region, the government usually only allows one set of natural gas distribution system.

The result is that companies who own infrastructure assets like toll roads and natural gas distribution systems operate like virtual monopolies.

If you want to earn a reliable stream of dividends, few sectors can do a better job than these companies.

Of course, infrastructure assets are expensive to build. But here’s the thing: once up and running, the cost needed to operate these assets are usually minimal compared to the construction costs.

Again, let’s use toll roads as an example. A toll road takes a lot of capital—and usually a long tim—to build. But once its built, the company who operates the road can simply collect money from each vehicle that uses it. There will be maintenance costs, but they are insignificant compared to the amount of cash the company is collecting from the travelers.

That’s why I’m not talking about companies that build infrastructure assets. The virtual monopolies I’m referring to are companies that own and operate these assets.

Brookfield Infrastructure Partners L.P. (NYSE:BIP) is a good example of a virtual monopoly business.

Brookfield Infrastructure Partners L.P.

Headquartered in Toronto, Ontario, Canada, Brookfield Infrastructure Partners L.P. owns and operates a diversified portfolio of infrastructure assets.

The company has four main operating segments: Utilities, Transport, Energy, and Data Infrastructure. In other words, the company is a lot more diversified than a traditional utility.

Furthermore, these assets are diversified across the globe. For instance, the company has around 2,000 kilometers of natural gas pipelines in South America, 3,900 kilometers of toll roads in South America and India, and 37 port terminals in North America, Asia Pacific, and Europe.

The high barriers to entry of the industry—whether it’s from high replacement costs or regulatory protection—has allowed Brookfield to generate outsized cash flows year after year.

And while the infrastructure business is not exactly known for its growth, the business’ financials have been consistently improving.

In 2009, Brookfield generated $0.69 per unit in funds from operations. By the third quarter of 2018, its annualized funds from operations per unit stood at $3.08. That came to a compound annual growth rate of 18%. (Source: “Q3 2018 Supplemental Information,” Brookfield Infrastructure Partners L.P., last accessed January 24, 2019.)

Also worth noting is that the company is determined to provide sustainable distributions to investors. So when a shareholder-friendly company generates a consistently increasing amount of cash, what would it do? Return that cash to investors.

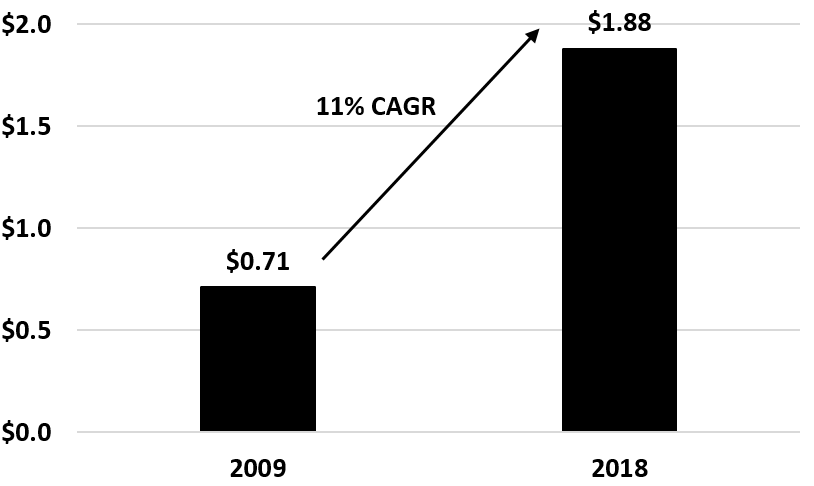

And indeed, that’s exactly what BIP has been doing. Look at the chart below. Over the last 10 years, BIP stock’s per-unit cash distribution had increased at a compound annual growth rate of 11%:

Brookfield Infrastructure Partners L.P. Per Unit Distribution Growth

Source: “Distribution History,” Brookfield Infrastructure Partners L.P., last accessed January 24, 2019.

The payout is also safe. In the first nine months of 2018, Brookfield Infrastructure Partners generated $2.31 per unit in funds from operations while declaring and paying total dividends of $1.41 per unit. (Source: “Brookfield Infrastructure Reports Third Quarter 2018 Results,” Brookfield Infrastructure Partners L.P., November 2, 2018.)

That translated to a payout ratio of just 61%, creating a wide margin of safety.

And don’t think for one second that the company is done with its payout increases. Going forward, management is targeting annual distribution growth of five to nine percent.

The Bottom Line on BIP Stock

No doubt, BIP stock is a great dividend growth stock.

And yet despite its solid business, the company hasn’t gotten much exposure in the financial media. After all, when was the last time you see the name Brookfield Infrastructure Partners L.P. in the headlines?

The reality is that most people are simply not that interested in the infrastructure business. They’d rather hear about a high-flying tech stock than a toll road operator.

And thanks to not being a hot ticker, BIP stock can still offer a decent yield.

Trading at $38.26 per unit, the company has an annual dividend yield of 4.9%.

For income investors, Brookfield Infrastructure Partners L.P. deserves a serious look.