Brookfield Infrastructure Partners L.P. Yields 4%

Can you name the one trait that AT&T Inc. (NYSE:T), General Mills, Inc. (NYSE:GIS), and Colgate-Palmolive Company (NYSE:CL) all have in common?

In short, these stocks have soldiered through some of the biggest economic crises in history. While many businesses have come and gone over the past century, these three firms have prospered. And in the process, they have created countless millionaires.

I have dubbed these kinds of companies “Forever Assets.” Regular readers know I have written about them many times before. In plain English, this is a set of stocks you can hold for the rest of your life. When you own them, you don’t have to worry about recessions, trade wars, or bear markets. If history is any guide, these firms will chug along paying out dividends to shareholders.

Today I bring you this group’s newest member: Canada-based Brookfield Infrastructure Partners L.P. (NYSE:BIP). Behind the scenes, this company’s management team has assembled a portfolio of trophy assets.

I can only think of two or three other companies in the world with such a collection of properties. And for investors, that should translate into a lucrative income stream.

A Dividend Stock to Consider Owning Forever

Now to be fair, Brookfield Infrastructure Partners L.P. doesn’t have the longest track record. Most Forever Assets have histories spanning decades or even centuries. This company, in contrast, only went public in 2008. That makes it a baby compared to other stocks in this category.

The short operating history doesn’t give us a lot of data to review, but in that short period, the company has acquired some of the most valuable assets on the planet. Brookfield executives have spent billions of dollars buying ports, pipelines, railroads, coal terminals, and toll roads. In more recent years, Brookfield has expanded into data centers and cell phone towers.

The company’s portfolio now spans five continents and sports a book value of $42.0 billion. (Source: “ Brookfield Infrastructure Partners: Rene Lubianski – Managing Director, Investments May 2019,” Brookfield Infrastructure Partners L.P., last accessed September 9, 2019.)

These assets represent the “beachfront properties” of the investment world. A new competitor can’t show up and build a rival business next door. For some of Brookfield’s operations, such as pipelines or toll roads, it doesn’t make sense to have two competitors in the market. In others, the government won’t grant the rights-of-way needed for new entrants. This leaves Brookfield with monopoly power over most of the customers it serves.

Savvy investment decisions boost the company’s returns further. CEO Sam Pollock often prunes the company’s portfolio, selling off underperforming businesses. He then plows those proceeds back into new assets that offer higher returns.

Since 2008, Brookfield executives have sold off $3.7 billion in assets. On average, these sales generate an internal rate of return of 25%. The strategy, in effect, turns the business into a giant capital recycling machine. It allows management to capture new opportunities without diluting unitholders.

For investors, this has produced tidy returns. Since 2008, Brookfield has made between $0.12 and $0.15 on every dollar of equity invested in the business. When you grow the book value of your company at that clip, it will show up in the stock price over time.

During that same period, Brookfield units have delivered a total return of 476%. That crushed the gain from the broader S&P 500, with much less risk.

Chart courtesy of StockCharts.com

Up 510%,With More Upside Ahead

Admittedly, Brookfield will have a tough time matching those returns going forward. In their search for income, private-equity firms have poured billions of dollars into infrastructure investments.

And with more money chasing fewer opportunities, asset prices have soared. That could make it harder for Brookfield to put new cash to work. Or worse, management may start overpaying for future deals. But technological changes have created more than enough demand for fresh capital.

The energy industry presents the big enchilada of opportunities. America’s fracking boom has unlocked vast supplies of oil and natural gas. It has also sparked a shortage of the facilities needed to ship, store, and process these supplies.

To meet demand, Brookfield estimates that the industry will need to invest $150.0 billion in the U.S. through 2021. Management has positioned themselves right in the middle of this boom.

Since 2015, Brookfield has plowed $3.2 billion into its midstream energy business. This includes everything from pipelines and storage tanks to terminals and processing plants. (Source: ” Brookfield Infrastructure Partners: Rene Lubianski – Managing Director, Investments May 2019,” Brookfield Infrastructure Partners L.P., op. cit.)

Less sexy than drilling for oil and gas, for sure. These businesses, however, throw off steady income. They also make money no matter which direction energy prices go.

Telecom also looks promising. People have developed a bottomless appetite for consuming data over wireless networks. That demand looks poised to grow as more devices connect to the Internet.

Carriers have limited bandwidth to send and receive signals, so in response, they have been spending billions of dollars beefing up their mobile networks. Much of this investment has focused on adding thousands of broadcasting sites nationwide.

Brookfield has cashed in by buying hundreds of cell phone towers. Management leases out these properties to carriers. In exchange, mobile companies pay Brookfield steady rent payments.

And these properties mint money. Thanks to the demand for new broadcasting sites, cell phone tower rents have soared. A fully leased-out site now generates a 24% annual return on investment. (Source: “American Tower Corporation: An Overview Second Quarter 2019,” American Tower Corporation, last accessed September 8, 2019.)

And those profits grow each year as management raises rents.

The best bets, though, might still come from old-fashioned infrastructure projects. Deferred maintenance has rotted out the nation’s roads, bridges, and airports. The American Society of Civil Engineers estimates that basic infrastructure repairs will cost a combined $2.0 trillion. (Source: “2017 Infrastructure Report Card: Investment,” American Society of Civil Engineers, last accessed September 8, 2019.)

Cash-strapped governments, however, often don’t have spare funds. Many face looming pension payouts, which will only stretch budgets further. That means plenty of opportunities for private investors.

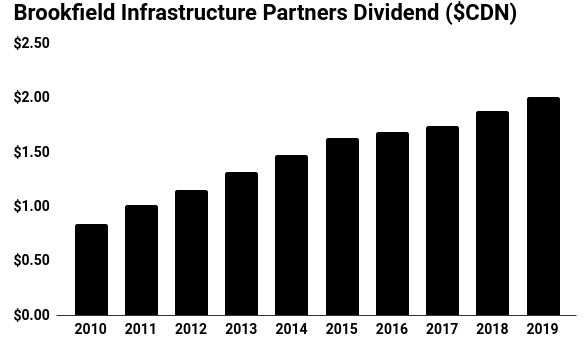

Nine Dividend Hikes (and Counting)

For Brookfield shareholders, this business has translated into a robust income stream. Over the past decade, management has boosted its payout at a 10% compounded annual clip. Today, units pay a quarterly distribution of more than $0.50 apiece, which comes out to an annual yield of 4.2%.

(Source: “Distribution History,” Brookfield Infrastructure Partners L.P., last accessed September 8, 2019.)

That payout looks poised to keep growing. Over the next decade, management aims to boost earnings by between 10% and 12% per year.

Much of that growth will come from new asset purchases. Brookfield also has a $1.1-billion backlog of construction projects at existing properties. That will provide plenty of cash to pay investors as those investments start to pad the bottom line. (Source: “Q2 2019 Supplemental Second Quarter,” Brookfield Infrastructure Partners L.P., June 30, 2019.)

If given enough time, this could balloon into quite the source of passive income. Let’s assume management continues to boost its distribution at a 12% annual clip. That rate looks modest, given the partnership’s tendency to under-promise. Regardless, this assumption puts Brookfield’s distribution at $7.00 per unit by 2030.

Based on today’s market price for Brookfield shares, that would raise the yield on cost to 14%. In other words, quite the income stream for anyone approaching retirement in a few years or so.

One Dividend Stock For the Next 100 Years?

In a nutshell, Brookfield Infrastructure Partners L.P. is a textbook Forever Asset. Since 2008, management has quietly accumulated a top-tier portfolio of infrastructure assets. Those properties should spin off growing dividends for decades to come.

My suggestion for long-term investors: consider scooping up shares of this Forever Asset, sticking the certificates in a drawer, and cashing the dividend checks for decades to come.