This Energy Stock Could Be a Long-Term Winner

One of the strategies that yield-seeking investors might want to consider is looking into the out-of-favor sectors of the stock market. Because stocks in these sectors haven’t really shot through the roof, some of them can offer much more substantial dividend yields than those in the hottest industries.

The energy sector would be a good example of this. Since the downturn in oil and gas prices started in the summer of 2014, many energy companies saw their business deteriorating. And stock market investors did not like that; in the last two and a half years, the S&P 500 Energy Index tumbled 24%.

And that index was made up of the relatively big players in the energy sector. For many small companies, things were even worse. Production cuts, layoffs, and dividend cuts weren’t uncommon. Some have shut down operations altogether.

However, if you take a closer look, you’ll see that not every company is deep in the doldrums. Over the past several months, a particularly generous dividend-paying energy stock has caught my attention: Blueknight Energy Partners LP (NASDAQ:BKEP).

Also Read:

7 Energy Stocks That Pay Healthy Dividends

Headquartered in Oklahoma City, Blueknight is a master limited partnership (MLP) that owns and operates midstream energy assets. The partnership does not make headlines very often, and because of its relatively small size (BKEP stock has a market capitalization of just over $200.0 million), most investors have never heard of it.

But in today’s market, Blueknight deserves income investors’ attention for a very simple reason: its oversized dividends. Right now, the average dividend yield of all S&P 500 companies stands at 1.8%. BKEP stock, on the other hand, is yielding a staggering 10.9%. (Source: “S&P 500 Dividend Yield,” Multpl.com, last accessed January 9, 2018.)

In other words, if an investor purchases Blueknight common units today, they would be locking in a yield more than six times the benchmark’s average.

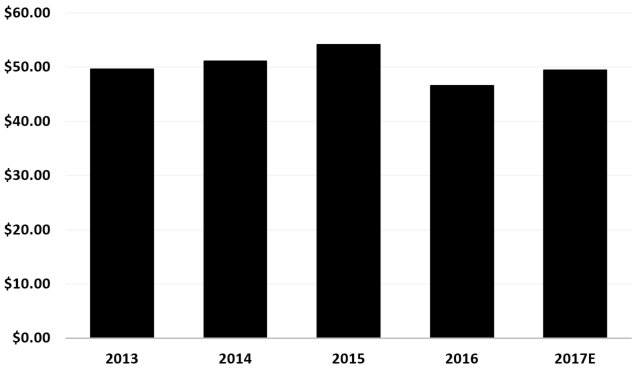

Of course, an ultra-high dividend yield like this could simply be a sign of trouble. The reason why I like BKEP stock is that despite being a small player in a rather volatile sector, the partnership actually runs a stable business. Just take a look at BKEP’s distributable cash flows for the past several years and you’ll see what I mean:

Distributable Cash Flow ($Millions)

(Source: “Investor Presentation,” Blueknight Energy Partners LP, last accessed January 9, 2018.)

Blueknight calculates its distributable cash flow by taking its adjusted earnings before interest, tax, depreciation, and amortization and subtracting cash paid for interest, maintenance expenditures, cash paid for taxes, and cash paid for fees related to acquisitions. The result is the cash that’s left available to be distributed to unitholders. In order for BKEP stock to pay distributions indefinitely, it needs to generate enough distributable cash flow from its operations.

As you can see from the chart, the partnership’s distributable cash flow has been relatively stable over the last few years. In particular, even with the massive downturn in commodity prices in the second half of 2014, Blueknight’s distributable cash flow actually improved year-over-year in both 2014 and 2015. The number dipped in 2016 but is expected to bounce back to between $48.0 million and $51.0 million for 2017.

Moreover, looking at BKEP’s financial results, the partnership’s cash flows are more than enough to meet its distribution obligations. Blueknight Energy Partners last reported earnings on October 31, 2017. In the third quarter of 2017, the partnership generated $16.6 million of distributable cash flow. Considering that it declared $12.3 million in total distributions during this period, BKEP achieved a payout ratio of 1.34 times, leaving a wide margin of safety. (Source: “Blueknight Announces Third Quarter 2017 Results and Anticipated Acquisitions,” Blueknight Energy Partners LP, October 31, 2017.)

In the first nine months of 2017, the partnership’s distribution coverage ratio was a less impressive 1.07 times, but it still means that Blueknight was generating enough cash to cover its payout.

In the long run, a management targets distribution coverage of between 1.0 times to 1.1 times.

The key to BKEP’s stable cash flows is its highly contracted operations. Product terminaling is by far the partnership’s biggest business. The business has two segments: asphalt terminaling services and crude oil terminaling services. On an annual basis, around 83% of BKEP’s asphalt terminaling services’ operating margins and 88% of its crude oil terminaling services’ operating margins comes from the fixed fee, take-or-pay contracts. This allows the partnership to minimize its commodity price exposure.

At the end of the day, there are stocks with even higher yields than Blueknight Energy Partners. But due to its stable business and solid cash flows, BKEP is one of the few double-digit yielders that is actually worth considering.