MO Stock Has Paid Dividends for 50+ Straight Years

The majority of large-cap blue-chip stocks generally yield less than five percent. But there are exceptions, and this is usually because a company’s share price is down due to operational issues.

Take the case of Altria Group Inc (NYSE:MO), a leading harvester and seller of tobacco in the U.S. and around the world. The company, which was established in 1822, is best known for its “Marlboro” brand. (Source: “Altria Group, Inc. (MO),” Yahoo! Finance, last accessed May 15, 2024.)

Altria stock has paid dividends for 54 straight years. It has also increased its dividends for the last 14 consecutive years. MO stock paid a quarterly dividend of $0.98 per share in January. (Source: “Dividend Information,” Altria Group Inc, last accessed May 15, 2024.)

As of this writing, that dividend represents a yield of 8.62%. (Source: Yahoo! Finance, op. cit.)

Its 10-year average dividend yield of 8.0% should entice income investors.

Altria Group Inc’s wonderful financial results should allow management to raise Altria stock’s dividends.

| Metric | Value |

| Dividend Growth Streak | 14 Years |

| Dividend Streak | 54 Years |

| 7-Year Dividend Compound Annual Growth Rate | 7.0% |

| 10-Year Average Dividend Yield | 8.0% |

| Dividend Coverage Ratio | 1.3 |

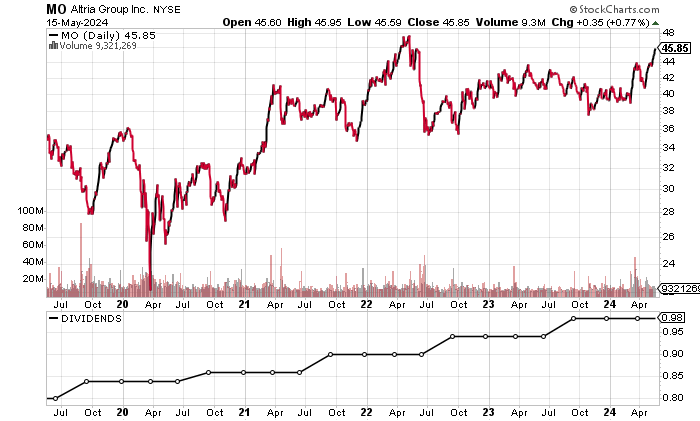

Moreover, MO stock’s price is up by 13.7% in 2024 (as of this writing) and has been outperforming the S&P 500 and the Nasdaq.

Chart courtesy of StockCharts.com

Steady Revenues & Massive Free Cash Flow at Altria Group Inc

Despite attacks on the tobacco industry from numerous governments, Altria has managed to grow its business. The company’s revenues increased for eight straight years, from 2014 to 2021, prior to making small drops in 2022 and 2023.

Analysts estimate that Altria Group Inc will report slight revenue growth of 1.3% to $20.77 Billion in 2024 and follow that with a 1.3% rise to $21.05 billion in 2025. (Source: Yahoo! Finance, op. cit.)

| Fiscal Year | Revenues (Billions) | Growth |

| 2019 | $19.8 | N/A |

| 2020 | $20.84 | 5.3% |

| 2021 | $21.11 | 1.3% |

| 2022 | $20.69 | -2.0% |

| 2023 | $20.5 | -0.9% |

(Source: “Altria Group, Inc,” MarketWatch, last accessed May 15, 2024.)

Altria has been generating strong gross margins. The company’s reading of 69.5% in 2023 was its highest gross margin in 10 years.

| Fiscal Year | Gross Margin |

| 2019 | 64.2% |

| 2020 | 64.7% |

| 2021 | 66.0% |

| 2022 | 68.6% |

| 2023 | 69.5% |

On the bottom line, Altria Group Inc generated generally accepted accounting principles (GAAP) profits for the last four straight years.

The company’s GAAP-diluted earnings-per-share (EPS) loss in 2019 was its only such loss in 10 years. Its GAAP-diluted EPS of $4.57 in 2023 was its highest since 2017 (and its third-highest since 2014).

Analysts expect the company’s adjusted earnings to rise to $5.10 per diluted share in 2024, compared to $4.95 per diluted share in 2023. They expect this to be followed with $5.30 per diluted share in 2025. (Source: Yahoo! Finance, op. cit.)

| Fiscal Year | GAAP-Diluted EPS | Growth |

| 2019 | -$0.70 | N/A |

| 2020 | $2.40 | 444.8% |

| 2021 | $1.34 | -44.3% |

| 2022 | $3.19 | 138.7% |

| 2023 | $4.57 | 43.2% |

(Source: MarketWatch, op. cit.)

Altria Group Inc’s funds statement shows the company churning out high free cash flow (FCF) over the last five years, with growth in three of the last four years. Its FCF of $9.09 billion in 2023 was its highest FCF in 10 years.

The company’s high FCF allows it to continue paying and raising its dividends.

| Fiscal Year | FCF (Billions) | Growth |

| 2019 | $7.59 | N/A |

| 2020 | $8.15 | 7.4% |

| 2021 | $8.24 | 1.1% |

| 2022 | $8.05 | -2.3% |

| 2023 | $9.09 | 12.9% |

(Source: MarketWatch, op. cit.)

On its balance sheet, Altria Group Inc had a debt of $26.2 billion at the end of 2023. This was partially offset by $3.72 billion in cash. (Source: Yahoo! Finance, op. cit.)

While the company’s debt load appears daunting on the surface, its profits, positive FCF, and ability to cover its interest payments mean the debt shouldn’t pose a problem.

The following table shows that Altria has managed to consistently cover its interest expenses via much higher earnings before interest and taxes (EBIT). Moreover, the company’s interest coverage ratio was a healthy 10.5 times in 2023.

| Fiscal Year | EBIT (Billions) | Interest Expense (Billions) |

| 2020 | $8.11 | $1.22 |

| 2021 | $5.01 | $1.19 |

| 2022 | $8.52 | $1.13 |

| 2023 | $12.08 | $1.15 |

(Source: Yahoo! Finance, op. cit.)

Altria Group Inc’s Piotroski score—an indicator of a company’s balance sheet, profitability, and operational efficiency—is a strong reading of 7.0. That’s just below the top of the Piotroski score’s range of 1.0 to 9.0.

The Lowdown on Altria Stock

In my view, Altria Group Inc is attractive and trades at a compelling valuation. MO stock is suited for income investors who desire consistent dividends and the potential for above-average share-price appreciation.

Altria has been stellar in returning capital to its shareholders. Since 2018, the company has bought back close to $7.0 billion worth of its own stock.

In 2023, the company bought back $1.0 billion worth of its own stock. (Source: “Altria Reports 2023 Fourth-Quarter and Full-Year Results,” Altria Group Inc, February 1, 2024.)