Top High-Yield Stock to Consider

In today’s market, a high dividend yield could simply be a sign of trouble. But this high-yield stock could be an exception.

I’m looking at Crestwood Equity Partners LP (NYSE:CEQP), a master limited partnership based out of Houston, Texas. The partnership owns and operates midstream energy assets located in the Marcellus Shale, Bakken Shale, Delaware Permian Basin, PRB Niobrara Shale, Barnett Shale, and Fayetteville Shale.

The number-one reason to consider Crestwood right now is to collect its generous dividends. Paying quarterly distributions of $0.60 per unit, the partnership offers an annual yield of nine percent at the current price.

As I mentioned earlier, high-yield stocks are usually not the safest bets. This is because if the company is solid and offers an attractive payout, investors will likely jump on the opportunity and bid up its price, thus lowering its yield. So if a stock’s yield stays high consistently, it could indicate some problems.

Also Read:

MLP Stock List: Earn Reliable Income From These Energy Partnerships

But for CEQP stock, there is a reassuring fact: the partnership boasts high insider ownership. According to Crestwood’s most recent investor presentation, the partnership’s insiders collectively own approximately 32% of all the outstanding limited partnership units. (Source: “Investor Presentation,” Crestwood Equity Partners LP, last accessed January 12, 2018.)

At any company, management always seems to be upbeat about their business. But when it comes to buying their own stock, not everyone is willing to put their money where their mouth is. Because of that, a high insider ownership can represent a much more genuine vote of confidence.

And because of their substantial stake in the business, management will be more likely to act in a way that benefits the partnership’s unitholders. As a matter of fact, CEQP ranked number one in Wells Fargo’s midstream investor alignment report, published in December 2017. (Source: Ibid.)

Other than significant insider ownership, this high-yield stock is also backed by a rock-solid business. Crestwood operates through three main segments: Gathering & Processing, Storage & Transportation, and Marketing, Supply & Logistics. In other words, even though the partnership comes from the volatile energy sector, its business is largely fee-based.

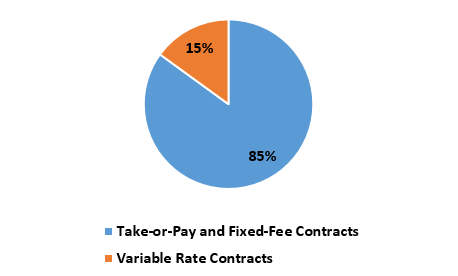

2017 Forecasted EBITDA

Source: Ibid.

The partnership is yet to report its fourth quarter results, but management expects that for full-year 2017, approximately 85% of its earnings before interest, tax, depreciation, and amortization (EBIDTA) would come from take-or-pay and fixed-fee contracts. This adds stability to the partnership’s cash flows.

At the same time, Crestwood also has a high-quality customer base. The company has been serving some of the industry heavyweights, including Royal Dutch Shell plc (NYSE:RDS.A), Exxon Mobil Corporation (NYSE:XOM), and Williams Companies Inc (NYSE:WMB).

And if you are concerned about this high-yield stock’s dividend safety, don’t worry. In the third quarter of 2017, Crestwood generated $50.3 million of distributable cash flow, which was 20% more than what it needed to pay in quarterly distribution. (Source: “Crestwood Announces Third Quarter 2017 Financial and Operating Results and Agreement to Sell U.S. Salt, LLC for $225 Million,” Crestwood Equity Partners LP, October 31, 2017.)

For those searching for a high-yield stock to add to their income portfolio, Crestwood Equity Partners deserves a serious look.