Collect Rock-Solid Dividends from This 5.3% Yielder

In today’s market, investors typically have to choose between income stocks and growth stocks. But these two sets don’t have to be mutually exclusive. For instance, one high-yield stock in the real estate sector is providing investors with both a handsome current payout and solid growth potential.

I’m looking at Brookfield Property Partners LP (NYSE:BPY), one of the largest global investors in real estate. The partnership owns and operates a huge portfolio that spans multiple asset classes, including office, retail, industrial, hospitality, multifamily, triple net lease, and self-storage assets.

Attractive Current Income

As a high-yield stock, it’s no surprise that Brookfield pays attractive current income. With a quarterly distribution rate of $0.295 per unit, the partnership has an annual dividend yield of 5.3%.

Brookfield Property Partners is a relatively new stock on the market, as it was spun off from Brookfield Asset Management Inc (NYSE:BAM) in March 2013. However, the partnership has already shown the ability to raise its payout. In just over four years, BPY stock’s quarterly distribution rate has increased by 18%. (Source: “Distributions,” Brookfield Property Partners LP, last accessed May 25, 2017.)

The partnership’s oversized dividends are backed by its rock-solid business. Brookfield owns and operates a high-quality portfolio, with office and retail being its core segments. Its core office segment consists of 146 premier office properties totaling 101-million square feet. These properties are located in gateway cities around the world, including New York, London, Toronto, Los Angeles, Sydney, and Berlin. They are 92% leased, with an average lease term of more than eight years.

One of the things that makes Brookfield stand out in office real estate is its diversified global structure. The partnership’s huge presence allows it to leverage relationships across geographies and industries. Among its top 20 office tenants, 13 lease from Brookfield in more than one city.

Like its office properties, Brookfield’s retail portfolio focuses on the best in class malls and urban retail properties. In the U.S., the partnership holds an interest in 127 retail assets totaling more than 125 million square feet. Same store retail occupancy at these properties was 95% by the end of the first quarter. Moreover, for leases beginning in 2016 to 2017, Brookfield’s core retail portfolio achieved average rent spreads of 20%, meaning the rent per square foot on new leases is 20% higher than the previous amount.

Core office and core retail currently make up 80% of the partnership’s balance sheet. The quality of these assets is key to the stability and durability of Brookfield’s cash flow.

The Best Is Yet to Come?

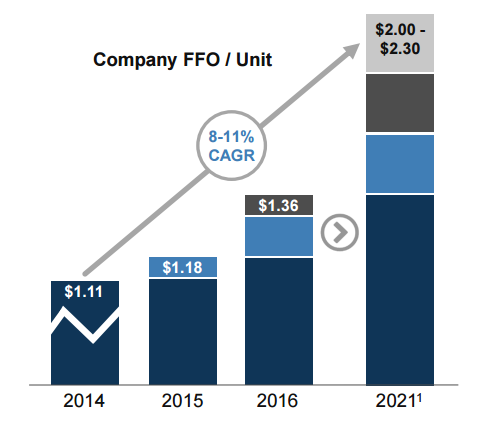

Other than current income, investors in this high-yield stock could also look forward to material growth in the future. Same-store growth is expected to be between two to three percent each year. Adding in contributions from the partnership’s active developments and reinvestment of capital at higher returns, Brookfield expects its funds from operations (FFO) per unit to increase at a compound annual growth rate (CAGR) of eight percent to 11% through 2021.

Source: “Corporate Profile,” Brookfield Property Partners LP, last accessed May 25, 2017.

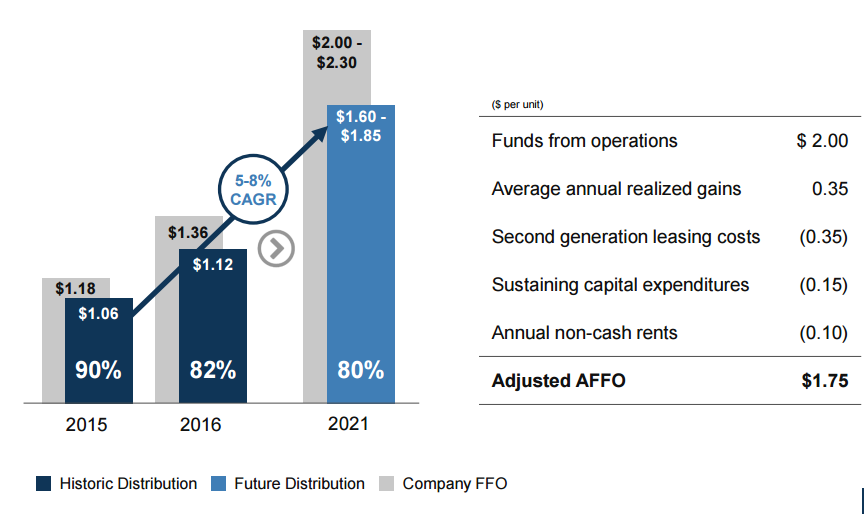

For a real estate stock, distributions come from the cash it generates. Having a growing stream of funds from operations is critical to future dividend increases. In the past, Brookfield always generated enough cash to cover its payout. Going forward, it is targeting an even more conservative payout ratio of 80%. Still, this would translate to an impressive annual compound growth of five to eight percent in its distributions through 2021.

Source: “Corporate Profile,” Brookfield Property Partners LP, last accessed May 25, 2017.

Conservative Financing Strategy

Other than current return and future outlook, investors in the real estate sector should also pay attention to a company’s financing strategy. Real estate assets are expensive, so companies often have to use a sizable amount of debt. With interest rates on the rise, will this high-dividend stock be able to handle the debt service burden?

Well, the good news is that Brookfield Property Partners usually borrows money in local currency and primarily with fixed interest rates. So whether it’s exchange rate fluctuations or interest rate hikes, the impact on the partnership’s financials would be limited.

Also Read:

10 Best Real Estate Stocks to Own in 2017

5 Cheap High Dividend Stocks for 2017

At the same time, note that the majority of Brookfield’s financing is done through asset-level, non-recourse debt. This means that while the loan is secured by a collateral (a property), the creditor cannot seek further compensation other than the collateral in the event of a default.

Don’t forget that Brookfield is one of the most solid real estate players in the market, with an investment grade corporate credit rating. Higher-rated companies typically have greater financial flexibility.

The Bottom Line on This High-Yield Stock

According to Brookfield, the partnership is currently trading at a significant discount to its International Financial Reporting Standards value. And based on its targeted distribution and earnings growth, the value of each unit of BPY stock would rise to $77.00 in the next 10 years. That would translate to a compound annual return of 13% for investors purchasing shares today.

Of course, it’s hard to predict whether the market will agree with Brookfield’s valuations in the future. But based on its sizable current payout and a rock-solid business, this high-dividend stock is already worth considering for income investors.